Money Made Simple

Feb 10, 2026

Top Financial Risks Creators Face (And How to Avoid Them)

Discover the top financial risks creators face, from income volatility to tax exposure, and learn how to build financial stability in the creator economy.

The creator economy looks exciting from the outside.

Brand deals. Viral growth. Digital product launches. Global audiences.

But behind the visibility, there is financial volatility that many creators are not prepared for.

Income can spike one month and disappear the next. Payments get delayed. Platforms change rules. Taxes catch people off guard. Collaborations break down over money disagreements.

The creators who last are not just creative. They are financially aware.

Understanding the top financial risks creators face is the first step toward building stability instead of stress.

1. Income Volatility

This is the biggest risk in the creator economy.

Unlike traditional employment, creator income is rarely predictable. It often depends on brand budgets, campaign cycles, platform algorithms, product launches, and seasonal advertising trends.

A strong month can create a false sense of security. A slow month can trigger panic.

Why This Is Dangerous

When creators increase their lifestyle during high-income months without planning for low-income months, financial pressure builds quickly.

You land a major brand deal worth $10,000. You upgrade your equipment, move to a better apartment, increase your spending baseline. Then next month brings in only $2,000. But your new expenses require $5,000. Suddenly you're operating at a deficit, not because you failed, but because you planned based on peak performance instead of average reality.

The absence of income smoothing is one of the fastest ways creators burn out.

How to Reduce This Risk

Track average monthly income over 6 to 12 months: Don't make decisions based on your best month or worst month. If you earned $60,000 over 12 months, your average is $5,000—even if individual months ranged from $2,000 to $15,000.

Identify your minimum monthly financial baseline: What is the absolute minimum you need to cover rent, essential utilities, food, transportation, insurance, and minimum debt payments? This is your survival number.

Avoid expanding expenses during peak months: When high-income months occur, resist lifestyle inflation. Instead, pay down debt, build emergency savings, or prepay fixed expenses.

Build a financial buffer for slow periods: The goal is to create 3 to 6 months of baseline expenses in reserve. This buffer transforms volatility from crisis to inconvenience.

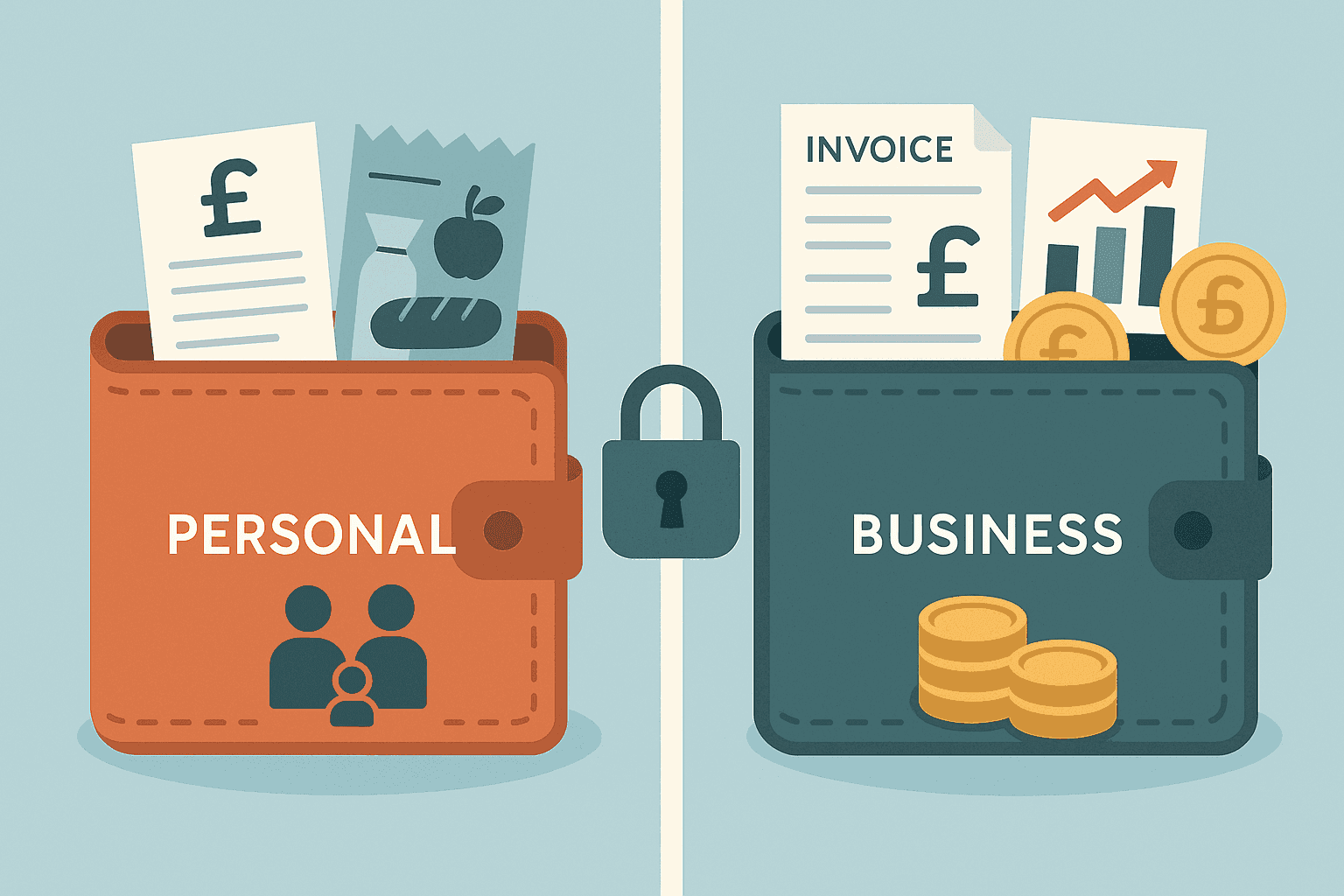

2. Mixing Business and Personal Finances

This is one of the most common structural mistakes.

Creators often receive payments into personal accounts and spend from the same pool. The result: no clear profit visibility, difficulty calculating taxes, emotional spending decisions, and inaccurate business performance tracking.

When everything blends together, clarity disappears.

What Mixed Finances Create

A typical creator's bank account shows brand payments, grocery shopping, digital product sales, rent, affiliate commissions, dinner expenses, and subscription fees all mixed together. After a month, the balance is higher than before, so they feel successful.

But they have no idea how much they actually earned from their business, how much they spent on business expenses, what their real profit margin is, how much they should set aside for taxes, or whether their business is growing or shrinking.

Beyond the practical problems, mixed finances create constant mental clutter. You're always doing informal math in your head. "Can I afford this?" requires calculating backward through multiple transactions. This uncertainty creates decision-making paralysis.

How to Reduce This Risk

Separate business income from personal spending: Open a dedicated business account. All creator income flows into this account. All business expenses come out of this account. Your personal account receives a regular "paycheck" from your business account.

Pay yourself intentionally: Rather than pulling money whenever needed, establish a consistent payment schedule. Calculate your average monthly business income, determine a sustainable salary, and transfer this amount on a set schedule.

Track expenses monthly: Review your business account at least once per month. Categorize expenses: operating costs, production costs, marketing, professional development, and administrative fees.

Understand your operating costs: Calculate your total monthly business expenses. This is your baseline—the amount you must earn just to break even before paying yourself.

3. Tax Exposure

As creator income grows, tax obligations grow too.

Many creators ignore tax planning, fail to track deductible expenses, mix taxable and non-taxable income, and wait until filing deadlines. This leads to sudden, large obligations.

Why This Is Risky

The typical scenario: A creator has a breakthrough year earning $80,000 from various sources. Money flows in throughout the year. They spend most of it on living expenses and business growth.

Tax season arrives. They discover they owe $24,000 in taxes—30% of their gross income. But they only have $5,000 in their account. Now they face inability to pay the full amount, payment plans with penalties and interest, potential credit damage, and stress that undermines their creative work.

Creator income creates unique tax challenges. Multiple income sources may have different tax treatment. Self-employment tax adds roughly 15.3% on top of income tax. Quarterly estimated payments are required if you expect to owe more than $1,000. Missing these creates penalties.

How to Reduce This Risk

Set aside a percentage of income for taxes immediately: Open a separate savings account specifically for taxes. Every time money enters your business account, transfer 25-30% to your tax savings account immediately. Treat this money as already spent.

Keep consistent records throughout the year: Track all income by source and date, all business expenses with receipts, mileage for business travel, home office percentage if applicable, and equipment purchases.

Make quarterly estimated payments: Calculate estimated taxes quarterly and pay on time. This prevents large lump-sum obligations and penalties.

Work with a tax professional: Once your creator income exceeds $30,000-$50,000 annually, professional tax help almost always costs less than the money saved through proper deductions and planning.

4. Lack of Emergency Savings

Many creators operate without a financial safety net.

Without savings, even small disruptions create instability: equipment breakdown, health issues, platform suspension, delayed brand payments, algorithm changes, economic downturns, or family emergencies.

An emergency fund is not optional in a volatile income model.

Why Emergency Funds Matter More for Creators

Traditional employees have predictable income, employer-provided health insurance, paid sick leave, unemployment insurance, and retirement contributions. Creators have none of these by default.

Your income depends entirely on your ability to create content consistently. Any disruption to that ability is a direct income threat. Without savings, each emergency becomes a financial crisis that compounds the underlying problem.

Lack of emergency savings also creates constant background anxiety. Even when things are going well, there's persistent worry: "What if something goes wrong?" This anxiety affects decision-making—you accept lower-paying work out of scarcity fear, avoid creative risks, and experience chronic stress.

How to Reduce This Risk

Build at least 3 to 6 months of essential expenses in savings: Calculate your essential monthly expenses: housing, utilities, food, transportation, insurance, minimum debt payments, and critical business expenses. Multiply by 3 to 6 months.

Treat savings as a fixed monthly priority: Don't save "whatever's left over." Save first, spend second. Set up automatic transfers from your business account to a dedicated savings account.

Protect high-income months by allocating surplus intentionally: When you have an exceptional month, don't increase spending proportionally. First top up emergency savings, then set aside extra tax reserves, then pay down debt, then invest in business growth.

Keep emergency savings separate and accessible: Use a high-yield savings account that's not linked to your everyday spending accounts.

5. Underpricing and Profit Illusion

Many creators underestimate their true costs.

They price based on what feels fair or what others charge, not based on time investment, production costs, software subscriptions, equipment, taxes, and team support. This creates the illusion of profit.

Revenue may look high, but actual take-home earnings are much lower.

The Real Cost of Creating

Consider a creator who charges $2,000 for a sponsored Instagram post. The actual breakdown reveals: 10 hours of work (research, shooting, editing, communication, revisions), $240 in direct and indirect costs (props, equipment depreciation, software, utilities), and $600 set aside for taxes.

Net income after all costs: $1,060. Effective hourly rate: $106.

This is decent—but if the creator thought they were earning $200 per hour based on just time investment, they're dramatically overestimating profitability.

Underpricing doesn't just reduce profit—it creates cascading problems. When you underprice, you must take on more clients to hit income goals, leading to more work, less creative space, and faster burnout. Lower prices can signal low value to brands. And once you establish low prices, increasing rates creates friction.

How to Reduce This Risk

Track all monthly expenses comprehensively: Include fixed costs, variable costs, equipment depreciation, and administrative overhead.

Calculate real operating costs: Add up all business expenses and divide by number of working hours available. This is your baseline cost per hour before profit.

Include tax considerations in pricing: Set aside at least 25-30% of gross income for taxes immediately. If you want $1,000 take-home from a project, you need to price at least $1,430 before taxes.

Review profit margins quarterly: Calculate total revenue, total expenses, and net profit. Healthy profit margins for creators typically range from 40-60%. If you're below 30%, you're underpricing or overspending.

6. Lack of Financial Visibility

Perhaps the biggest hidden risk is simply not knowing.

Creators often cannot clearly answer: How much did I earn last month? How much did I actually keep after expenses? What is my average monthly income? Which revenue stream performs best? Am I profitable?

Without visibility, decisions are emotional. With visibility, decisions are strategic.

What Lack of Visibility Looks Like

A creator checks their bank balance. It's $8,000, higher than last month's $6,000. They feel successful.

But they can't actually answer how much revenue came in, how much went to business expenses versus personal spending, how much should go to taxes, or whether that $2,000 increase is profit or just timing of income versus expenses.

Without data, they can't make informed decisions. A brand offers $1,500 for a campaign. They don't know if this is fair because they don't know their current average deal size, profit per campaign after costs, effective hourly rate, or whether they have capacity at this rate.

Why Visibility Matters

Visibility provides confidence in decision-making. When you know your numbers, you can say yes or no to opportunities based on real criteria, not anxiety.

It reveals patterns: which months are typically slow, which income streams are growing versus declining, which expenses deliver return on investment, and which activities actually generate revenue.

It enables strategic planning. Without visibility, you can't set realistic goals or make informed growth decisions.

Most importantly, visibility replaces vague worry with concrete problems you can solve.

How to Reduce This Risk

Create a simple monthly financial review habit: Block 1-2 hours at the end of each month to review total income received, total expenses paid, net profit, bank balance, and outstanding invoices.

Track income by source: Don't just record total income. Categorize by brand partnerships, digital products, affiliate revenue, ad revenue, and consulting. This reveals which streams actually drive your income.

Calculate your monthly burn rate: What are your total monthly operating costs? This is how much you need to earn just to break even before paying yourself.

Establish clear metrics you check regularly: monthly revenue, monthly net profit, average income per brand deal, profit margin percentage, and month-over-month growth rate.

Use tools that centralize financial information: Create a single place where financial information lives. Scattered information across multiple accounts and platforms makes visibility impossible.

Why Financial Infrastructure Matters

Most financial risks in the creator economy stem from poor visibility and lack of structure.

The solution isn't working harder or earning more—it's building systems.

Creators need infrastructure that allows them to see income clearly across all sources, separate business from personal spending automatically, track product revenue without manual spreadsheets, understand monthly performance at a glance, and plan ahead based on real data.

Financial awareness is not about restriction. It is about control.

When you have financial clarity, pricing becomes strategic not emotional, growth planning becomes possible not theoretical, stress reduces because uncertainty decreases, and professional confidence increases because you understand your business.

Most creators never achieve their potential not because they lack talent, but because they lack financial structure.

How Endow Helps Reduce Creator Financial Risk

Endow is built for creators who want structure without complexity.

Traditional banking doesn't understand creator income. Business accounts designed for traditional companies don't fit creator needs. Personal accounts create the mixing problems we've discussed.

Endow provides creator-specific financial infrastructure:

Centralize digital product income across platforms

Track creator earnings holistically in one place

Separate business and personal finances automatically

Build predictable financial systems with automated tax reserves

Plan based on real numbers with clear profit visibility

Manage storefront income professionally

When money is organized, stress reduces. When stress reduces, creativity improves.

Final Thoughts

The creator economy offers opportunity. It also carries risk.

Ignoring financial risks does not make them disappear. It makes them more expensive.

Income volatility, mixed finances, tax exposure, missing savings, underpricing, and financial invisibility—these risks compound over time.

The creators who build lasting careers are not just talented. They are structured.

If you understand the risks, you can design infrastructure that protects you.

And when your foundation is stable, growth becomes intentional, not chaotic.

Structure is not the opposite of creativity. Structure is what enables creativity to scale.

Related Content